AI, SWIFT & The Coming Trust Crisis

Financial Stability Risks in the Age of Machine-Speed Adversaries

The recent IMF warning regarding artificial intelligence and financial stability risks is not merely a cybersecurity concern.

It is a warning about the possible collapse of trust within the coordination layer of the global financial system.

The danger is not simply:

- banks being hacked,

- fraudulent transfers,

- or isolated cyber incidents.

The deeper risk is that artificial intelligence fundamentally changes the nature, scale, speed, and coordination capability of adversarial activity against systems that were designed for a completely different era.

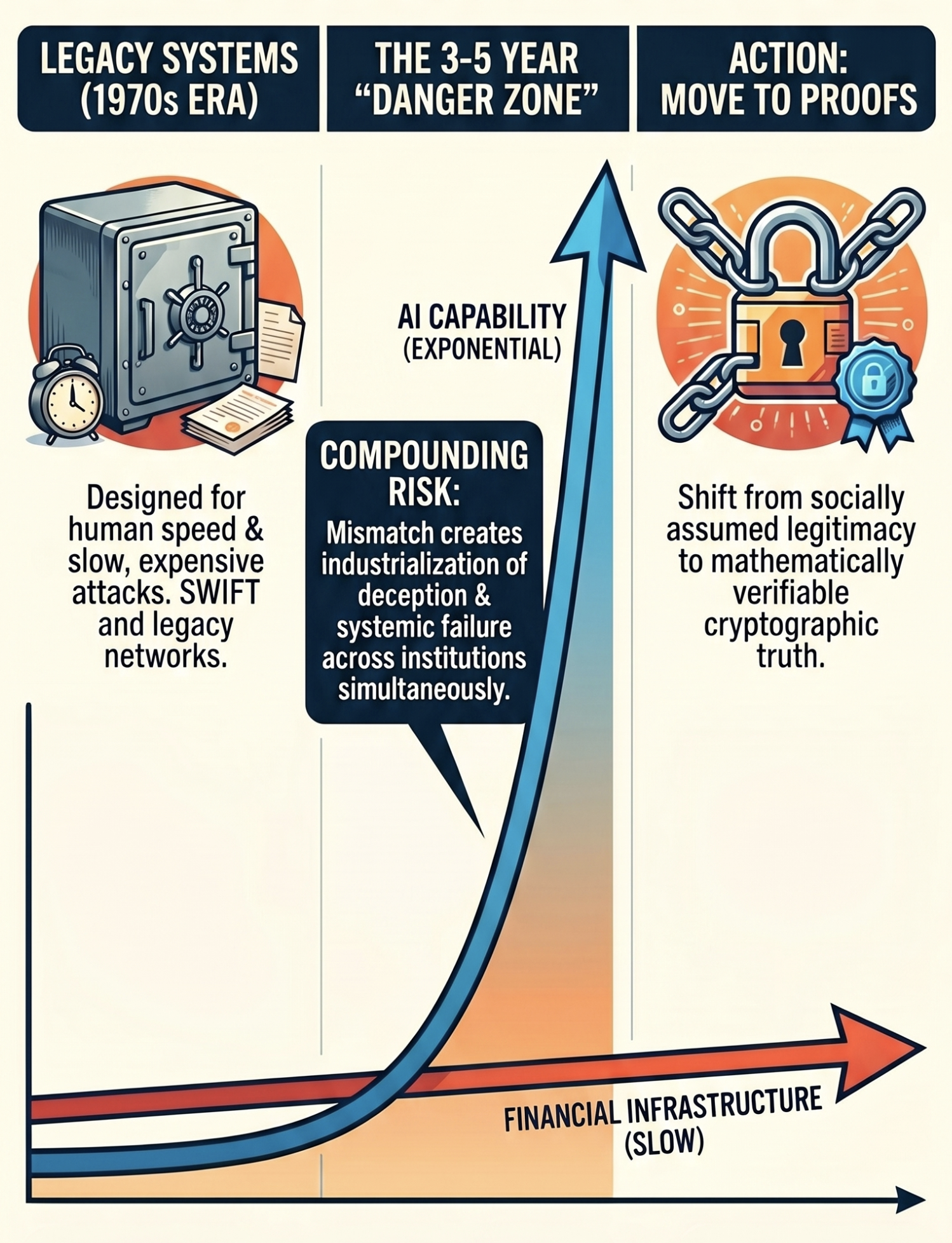

The SWIFT network represents one of the clearest examples of this mismatch.

Built in the 1970s, SWIFT emerged in an age where:

- institutions were slower,

- attacks were expensive,

- humans operated systems directly,

- and trust assumptions were fundamentally institutional.

Artificial intelligence changes all of these assumptions simultaneously.

The result is not merely an increase in cyber risk.

It is the emergence of systemic trust instability.

The SWIFT Network Was Designed for Human-Era Finance

SWIFT was created to solve a major coordination problem:

How can financial institutions exchange trusted settlement instructions globally?

Importantly:

- SWIFT does not move money directly.

- SWIFT moves trusted messages about money.

This distinction matters enormously.

The global banking system relies on assumptions such as:

- messages are authentic,

- counterparties are legitimate,

- institutions behave rationally,

- and operational processes remain trustworthy.

The system assumes that:

- authentication implies legitimacy,

- operational timing is human,

- fraud is sparse,

- and attacks are relatively isolated.

These assumptions were reasonable in a human-limited world.

They become dangerous in an AI-enabled world.

AI Removes the Human Bottleneck

Historically:

- attacks required human coordination,

- reconnaissance took time,

- exploits were manually developed,

- social engineering was labor intensive,

- and fraud detection depended heavily on human review.

Artificial intelligence changes the economics completely.

AI systems can:

- scan infrastructure continuously,

- identify vulnerabilities rapidly,

- generate adaptive phishing campaigns,

- mimic institutional communication,

- automate exploit generation,

- analyze operational responses,

- and recursively refine attack strategies.

This is not merely “automation.”

It is the industrialisation of adversarial capability.

The bottleneck is no longer human effort.

The bottleneck becomes compute and access.

The Real Risk Is Correlated Failure

Traditional cybersecurity thinking assumes:

- local failures,

- isolated breaches,

- and recoverable incidents.

AI changes cyber risk into a systemic coordination problem.

Modern financial infrastructure is highly concentrated around:

- shared cloud providers,

- shared authentication systems,

- shared operational vendors,

- shared software frameworks,

- and shared trust protocols.

This means vulnerabilities are increasingly correlated.

Instead of:

- one institution being compromised,

AI enables scenarios where:

- hundreds of institutions discover simultaneous exposure.

The issue is no longer:

“Can a bank survive an attack?”

The issue becomes:

“Can the financial system maintain confidence during simultaneous uncertainty?”

That is a fundamentally different category of risk.

SWIFT’s Weakest Layer Is Trust

SWIFT fundamentally depends on trusted institutional signaling.

Its model is effectively:

“We trust the sender institution.”

But artificial intelligence increasingly undermines confidence in:

- sender authenticity,

- operational legitimacy,

- communication integrity,

- and human verification.

AI-generated communications can now:

- replicate executive tone,

- reproduce operational language,

- mirror transaction timing,

- simulate counterparties,

- and create highly plausible settlement instructions.

The danger is not merely fraudulent messages.

The danger is uncertainty about whether any message can be trusted.

Once trust in signaling weakens:

- settlement slows,

- counterparties hesitate,

- liquidity freezes emerge,

- collateral demands increase,

- and systemic stress amplifies.

Financial systems are ultimately:

- synchronized trust systems.

The moment participants lose confidence in the shared informational state, instability accelerates rapidly.

Human Verification No Longer Scales

Historically, suspicious activity could be escalated to humans.

Fraud detection often relied on:

- intuition,

- anomalies,

- unusual wording,

- or timing inconsistencies.

Artificial intelligence weakens all of these mechanisms.

AI systems can:

- generate near-perfect operational mimicry,

- adapt to institutional behavior,

- learn communication patterns,

- and continuously refine social engineering attacks.

Humans become too slow relative to machine-speed interaction.

This creates a dangerous transition point:

- systems increasingly rely on machine-generated verification,

- while adversarial systems are also machine-generated.

The system begins trusting synthetic signals produced by other synthetic systems.

At that point:

- humans are no longer governing trust,

- they are merely supervising machine interactions they cannot fully audit in real time.

The Next Financial Crisis May Be Informational

Historically, financial crises were often:

- liquidity crises,

- leverage crises,

- or credit crises.

The AI era introduces the possibility of:

- informational crises.

Examples include:

- synthetic executive instructions,

- falsified treasury operations,

- manipulated liquidity indicators,

- corrupted dashboards,

- poisoned AI models,

- fake counterparty distress,

- and AI-generated market narratives.

Modern finance depends heavily on:

- informational coherence.

Artificial intelligence directly attacks coherence itself.

This is why the risk is larger than “cybersecurity.”

The issue becomes:

“Can institutions maintain a shared trusted reality?”

Legacy Infrastructure Contains Embedded Assumptions

The age of SWIFT matters because old systems embed old assumptions.

These assumptions include:

- humans are the primary operators,

- institutions are difficult to impersonate,

- attacks are expensive,

- trust propagates hierarchically,

- and verification can occur slowly.

Artificial intelligence invalidates these assumptions simultaneously.

The problem is not that SWIFT is “old.”

The problem is that:

- it was optimized for human-scale adversaries,

- not autonomous machine-scale adversaries.

The Shift From Institutional Trust to Cryptographic Trust

The AI era increasingly pushes financial systems toward:

- cryptographic verification,

- hardware-backed identity,

- immutable event logs,

- zero-knowledge proofs,

- verifiable credentials,

- and machine-verifiable state transitions.

The old paradigm was:

trusted institutions.

The emerging paradigm becomes:

trusted proofs.

This represents a profound architectural shift.

In a world of synthetic intelligence:

- reputation becomes insufficient,

- authentication becomes insufficient,

- and institutional identity becomes insufficient.

Systems increasingly require:

- mathematically verifiable truth,

- not socially assumed legitimacy.

The Strategic Question

The critical question is no longer:

“Can banks stop hackers?”

The deeper question is:

“Can human-era trust architectures survive machine-era adversaries?”

This is not simply a technical issue.

It is a civilisational coordination problem.

Because finance itself is ultimately:

- a system of synchronized belief,

- operational trust,

- and coordinated informational reality.

Artificial intelligence introduces the possibility that:

- synthetic systems can manipulate those realities faster than humans can verify them.

Conclusion

The IMF warning should not be interpreted narrowly as:

- “AI increases cyber risk.”

The deeper implication is:

- AI destabilizes the assumptions underpinning institutional trust systems.

SWIFT represents a symbolic example of this challenge:

- a globally critical coordination layer,

- built for a slower human era,

- now exposed to machine-speed adversaries.

The real danger is not merely theft.

The real danger is:

- uncertainty,

- hesitation,

- informational incoherence,

- and loss of confidence in settlement integrity itself.

The next generation of financial infrastructure will likely require:

- cryptographic verification,

- machine-native trust architectures,

- verifiable identity systems,

- immutable auditability,

- and continuously validated state transitions.

The future financial system may increasingly resemble:

- a distributed cryptographic trust network, rather than:

- a hierarchy of trusted institutions.

The AI era does not merely challenge cybersecurity.

It challenges the foundations of institutional trust itself.