How Long Will It Take to Fix the AI vs Financial System Risk?

The Short Answer

Potentially decades.

Not because the technology is impossible.

But because global financial trust infrastructure evolves extremely slowly.

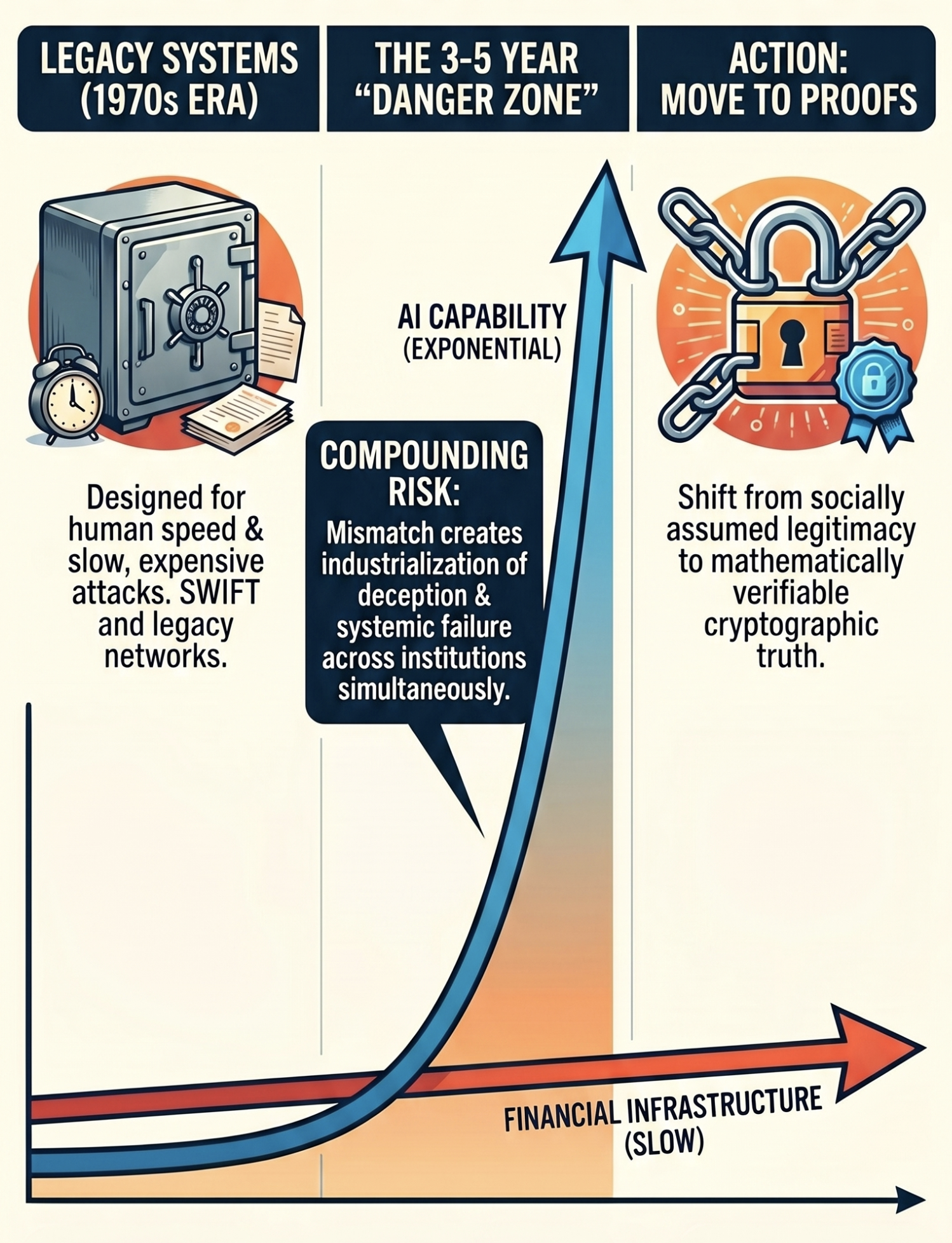

SWIFT itself is a good example:

- founded in 1973

- deeply embedded into global banking

- connected to thousands of institutions

- still carrying assumptions from the pre-internet era

Financial systems optimise for:

- stability

- compatibility

- regulatory certainty

- operational continuity

Not rapid innovation.

The Core Problem

Artificial Intelligence capability is compounding exponentially.

Financial infrastructure evolves linearly.

This creates a widening capability gap.

AI capability growth = exponential

Financial adaptation = bureaucratic/incremental

The danger zone is the expanding gap between those two curves.

The Next 3–5 Years: The Most Dangerous Period

This is likely the highest-risk phase.

Why?

Because:

- AI attack capability is rapidly improving

- while financial systems remain heavily human-governed

Expect:

- AI-enabled fraud at industrial scale

- synthetic identity attacks

- executive impersonation

- deepfake operational instructions

- AI-generated phishing

- automated vulnerability discovery

- insider-style attacks without insiders

The initial industry response will likely be:

- more monitoring

- more AI security tooling

- increased cyber spending

- tighter regulation

But these are mostly defensive layers added onto old trust models.

The Real Fix Requires Rebuilding the Trust Layer

The deeper problem is not merely cybersecurity.

It is the structure of trust itself.

Modern financial systems were designed around:

- institutional trust

- human verification

- slow-moving operations

- assumption-based authentication

AI destabilises all four.

The long-term solution likely requires systems based on:

- cryptographic identity

- hardware-backed authentication

- signed machine actions

- verifiable event logs

- deterministic auditability

- zero-trust architectures

- machine-verifiable state transitions

This is not a patch.

It is a redesign of financial coordination infrastructure.

Why This Takes So Long

1. Global Compatibility Constraints

Finance is interconnected.

You cannot simply say:

“Tomorrow we replace SWIFT.”

Every:

- bank

- central bank

- clearing house

- treasury

- regulator

- correspondent network

- sanctions framework

- compliance system

must continue interoperating.

This creates enormous inertia.

2. Regulation Moves Slowly

Regulators are still adapting to:

- cloud infrastructure

- APIs

- open banking

- digital assets

- AI governance

AI-native financial risk is newer still.

Regulators must avoid destabilising the system while modernising it.

Therefore they move cautiously.

3. Institutions Resist Core Infrastructure Change

Large institutions generally:

- layer new controls onto old systems instead of:

- redesigning foundations

Why?

Because redesigning core banking infrastructure is operationally terrifying.

The incentives strongly favour:

- continuity

- incrementalism

- risk minimisation

This results in:

- AI security wrappers around

- legacy trust assumptions

4. Human Governance Is the Bottleneck

Ironically, the largest scalability problem is human coordination itself.

Examples:

- committees

- procurement cycles

- legal negotiations

- regulatory reviews

- governance processes

- cross-border agreements

- board approvals

Machine-speed adversaries are colliding with quarter-by-quarter governance systems.

The Likely Evolution Path

The future probably does not look like:

- one giant replacement event

Instead, it likely evolves in layers.

Phase 1 — AI Defensive Arms Race (Now)

Current focus:

- AI vs AI cybersecurity

- anomaly detection

- fraud monitoring

- deepfake detection

- behavioural analytics

- automated incident response

This phase attempts to defend existing systems.

Phase 2 — Cryptographic Hardening

Likely developments:

- hardware-backed signing

- mTLS everywhere

- machine identity frameworks

- secure enclaves

- signed infrastructure actions

- verifiable attestations

This phase strengthens trust boundaries.

Phase 3 — Verifiable Financial Coordination

Possible developments:

- cryptographically provable settlement

- signed event chains

- deterministic reconciliation

- real-time auditability

- programmable compliance

- verifiable institutional workflows

This phase changes how trust itself is represented.

Phase 4 — Machine-Native Financial Systems

Potential future:

- autonomous treasury systems

- AI-managed liquidity

- machine-verifiable institutions

- programmable regulation

- cryptographic trust fabrics

- continuously verified settlement systems

This phase could take:

- 10–30 years

Possibly longer globally.

The Deep Structural Issue

The issue is not merely:

“old software.”

The issue is:

“human trust architecture.”

SWIFT is fundamentally a social coordination system encoded into software.

AI changes:

- the economics of deception

- the scale of impersonation

- the speed of adversarial action

- the cost of intelligence

- the feasibility of synthetic trust

Systems built around:

- institutional reputation and

- human verification

must gradually evolve toward:

- cryptographic verification

- machine-verifiable truth

- deterministic trust systems

The Most Important Insight

The next major transformation in finance is probably not:

- digital banking

- mobile payments

- cryptocurrency

- AI automation

It is likely:

The transition from institution-based trust to cryptographically verifiable trust.

That transition may become one of the largest infrastructure migrations in financial history.

And the most dangerous period is likely not after the transition.

It is during the transition itself.

References

- SWIFT Overview

https://www.swift.com